A budget is not a cage; it is a map. It doesn’t tell you what you can’t do, but rather shows you what is possible when every dollar you earn is given a specific mission.

In 2026, budgeting has evolved far beyond the traditional shoebox of receipts or even a simple spreadsheet. With the rise of real-time digital payments, subscription-based economies, and fluctuating costs of living, a static budget is no longer enough. Long-term financial health requires a dynamic, principles-based approach that adapts to your life while keeping your long-term goals non-negotiable.

Building on our previous discussion about financial stability, budgeting is the daily operational manual that makes stability possible. It is the bridge between your current income and your future freedom. In this comprehensive guide, we will explore the most effective budgeting frameworks for the modern age, from the classic 50/30/20 rule to the precision of zero-based budgeting.

The 50/30/20 Framework: The Golden Ratio of Personal Finance

For those starting their journey or looking for a sustainable long-term model, the 50/30/20 rule remains the gold standard. It provides a clear structure that balances immediate needs with future growth without sacrificing the quality of life.

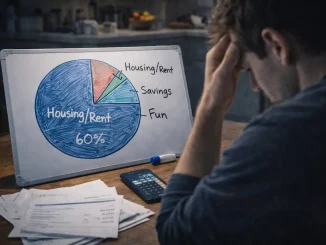

- 50% for Needs: Housing, utilities, groceries, and minimum debt payments. If this exceeds 50%, it’s a signal that your “fixed costs” are too high for your current income.

- 30% for Wants: Dining out, travel, subscriptions, and hobbies. This is your “lifestyle” category that provides flexibility during tight economic months.

- 20% for Financial Goals: Debt overpayments, emergency funds, and long-term investments. This is the only category that actually builds your net worth.

🚀 The 2026 Optimization: The 40/20/40 Pivot

In high-income brackets or periods of intense wealth-building, aggressive savers are pivoting to a 40/20/40 model—capping needs and wants to maximize the 40% going into high-yield assets and retirement accounts. This is the fastest way to achieve “Financial Independence.”

Zero-Based Budgeting: Giving Every Dollar a Job

If the 50/30/20 rule is a map, Zero-Based Budgeting (ZBB) is a GPS. At the start of every month, your Income minus Expenses must equal Zero. This doesn’t mean you have zero dollars in your bank account; it means every single cent is allocated to a category (including savings and “fun money”).

This method is exceptionally powerful for stopping “invisible leaks” like forgotten subscriptions or impulse digital purchases. According to recent consumer behavior studies, individuals who use ZBB find an average of 15-20% more “hidden” cash in their existing income simply by eliminating waste.

⚠️ Warning: The Subscription Trap

In 2026, the average household pays for 12+ digital subscriptions. These “micro-leaks” are the enemy of long-term health. Audit your digital wallet monthly and use the “One-In, One-Out” rule for entertainment services.

Budgeting for “True Expenses”: Avoiding the Sinking Fund Crisis

Most budgets fail because they only account for monthly recurring bills. They forget about the “predictable surprises”—the annual car insurance, the holiday gifts, or the home repair. This is where Sinking Funds come in.

A sinking fund is a dedicated savings category for a specific future expense. By breaking a $1,200 annual expense into a $100 monthly “budget item,” you turn a financial crisis into a non-event.

| Feature | Traditional Budgeting | Smart Budgeting (2026) |

|---|---|---|

| Focus | Tracking past spending. | Directing future wealth. |

| Tooling | Pen & Paper / Basic Sheets. | AI-driven apps & Automated flows. |

| Emergency Handling | Reactive (Credit cards). | Proactive (Sinking funds). |

| Goal | Survival / Paying bills. | Building long-term autonomy. |

The Role of Automation in Financial Health

Willpower is a finite resource. The smartest budgeters remove themselves from the equation through Automation. In 2026, your financial flow should look like a “waterfall”:

- Paycheck hits the account.

- Automatic transfer to Savings/Emergency Fund (Pay Yourself First).

- Automatic transfer to Investment accounts.

- Automatic payment of fixed bills.

- The remainder is your “Safe-to-Spend” amount.

Final Thoughts: Consistency Over Perfection

Smart budgeting isn’t about getting every cent right on day one. It’s about creating a system that reflects your values and keeps you moving toward your long-term goals. Whether you choose the simplicity of 50/30/20 or the precision of zero-based budgeting, the best system is the one you can stick to for the next decade.

A well-managed budget naturally creates a surplus, and that surplus is what builds your ultimate safety net. In our next article, we will take the next logical step in your personal finance journey: the importance of emergency funds in personal finance and how much you truly need to stay safe in 2026.

Frequently Asked Questions (FAQ)

What is the best budgeting app for 2026?

The “best” app depends on your style. For Zero-Based Budgeting, apps like YNAB (You Need A Budget) remain leaders. For Automation and AI-insights, many modern neo-banks offer built-in “Pockets” or “Buckets” that automatically categorize spending and suggest savings targets based on your history.

How can I budget with an irregular income?

Budgeting with a variable income (like freelancing) requires a “Hill and Valley” fund. In months where you earn more (Hills), you save the surplus. In months where you earn less (Valleys), you draw from that surplus to pay your “Baseline Budget”—which should only cover your absolute 50% “Needs.”

Does budgeting hurt my credit score?

Directly, no. However, indirectly, it is the best thing for your score. A budget ensures you never miss a payment and helps you keep your “Credit Utilization” low, which are the two biggest factors in your credit rating, as we discussed in our banking and credit series.

Should I budget for investments as an expense?

Yes. To reach long-term financial health, you must treat your future self as a “Bill” that must be paid every month. By listing your 401k, IRA, or brokerage contributions as a non-negotiable budget item, you guarantee your wealth grows regardless of lifestyle changes.

Be the first to comment